SilverDoor’s Market Update is a comprehensive review of the global travel landscape using our own booking data, wider economic context, and our experts' experience and predictions to build a picture of serviced apartment trends worldwide. Reflecting on the past quarter and forecasting for the year ahead, the report advises corporates on rates, supply, demand and traveller preference to inform booking practices.

SilverDoor captures more than 127,000 datapoints from an average of 593,000 enquired room nights each quarter, the largest and most extensive sets of data available in the sector. This means we can provide the most accurate trend commentary and forecasting for global mobility professionals.

_______________________________

|SilverDoor Snapshot

The general global trend we’re seeing is rates coming down due to a decline in travel in the second half of this year. Demand has slowed and global average daily rates (ADRs) have decreased 7.9% from £173.52 per night (May-July 2023) to £159.71 (August-October 2023), usual for the time of year but some markets will remain more stable than others.

The YoY decrease in global ADRs for one-bedroom apartments for the August-October period is less dramatic than it was for the May-July period (down 3.3% from £165.19 in August-October 2022 to £159.71 during the same period in 2023). However, there is a noticeable drop in rates compared to last quarter.

_______________________________

|Current Economic Landscape

Europe, Middle East & Africa

Europe, Middle East & Africa

In November, the Bank of England didn’t raise interest rates for the second consecutive month. This may have relieved many markets for now and lessened the recession risk, but interest rates remain at a 15-year high and a sluggish growth is still predicted for the UK economy.

Eurozone energy prices may have stabilised but are still historically high, and inflation is slowly reducing despite remaining above the central banks' target, which is usually around 2%. Oxford Economics predict Ireland, Romania and Luxembourg will lead economic growth in 2024 while Sweden, Germany and the UK anticipate the lowest GDP.

Dubai is developing a second Palm, Palm Jebel Ali, as part of their 2040 Urban Master Plan that’s projected to be twice the size of the current Palm Jumeirah. Planned to house 80 new hotel developments, this is further pushing Dubai as a strong investment opportunity and may result in higher demand and rate hikes.

A New Administrative Capital (NAC) is being built in Egypt to ease congestion in Cairo and improve the overall quality of life in the country. The NAC for Urban Development is set to be the size of Singapore and being developed to house all government and parliamentary activity, provide housing for the current overcrowded capital, and add green space to tackle pollution. This positions Egypt as a more attractive business travel destination and key EMEA player for accommodation investors going into 2024.

Geo-political tension is evident worldwide, posing a risk to the overall global economy. In Europe, the Ukraine/Russia war continues and conflict in Israel/Gaza begun in October. So far, the impact of the Israel/Gaza war on oil prices has been modest – especially compared to the initial consequences of the Russia/Ukraine war – but the extent of the market impact remains to be seen.

Rate Trends Across EMEA

There is a noticeable softening of rates across the EMEA market and rates are expected to be more competitive at the start of 2024, except in Paris where both demand and rates are soaring for July, August and the months either side of the 2024 Olympics. Advanced bookings aren’t as noticeable in other major cities and there has been a slight drop in demand throughout the Eurozone.

Except for Paris, the one-bedroom ADR we're currently seeing in our booking data across most major EMEA cities for January 2024 are on par with January 2023, if not lower:

Dubai ADR started the year averaging £132 but we're accessing inventory for the start of 2024 around the £115 mark.

ADRs in Egypt are up 15.4% from £159.34 (May-July 2023) to £183.91 (August-October 2023) indicating the increasing corporate appetite in the area.

London rates averaged £190 for stays in January 2023, but so far ADR is approximately 7% down for the same period in 2024 at around £177.

In Dublin, ADRs started 2023 at £154 but rooms are already selling for £136 at the start of 2024.

Amsterdam ADR was £154 in January 2024. Rates picked up and were considerably higher for most of the year, but latest trends indicate a slow fall and levelling out around the same point at year-end, with £155 being the ADR for January 2024.

![APAC globe icon]() Asia Pacific

Asia Pacific

Asia Pacific

Asia Pacific

India has overtaken China as the world’s most populous nation and Goldman Sachs predict the country will have the world’s second largest economy by 2025.

India has been seen to be investing healthily in infrastructure projects to move away from agriculture-based employment and towards business services. There is high demand for short-term housing in Bangalore, Mumbai and Hyderabad from software engineers and developers, financial analysts and project managers.

There’s a current economic slowdown in China with the Chinese yen weakening to its lowest level in 16 years. Consumption, production and investment have slowed and employment rates have fallen, although HSBC predict the country is over the worst of its real estate crisis.

China’s weakening yen has supported a growth in Japanese exports and a consequent rise in Japan’s real GDP. Inflation is still above the central banks' target and has been for seven consecutive months, according to Deloitte, but the Bank of Japan continues to keep inflation rates lower than other major economies.

Australia’s economy is likely to escape recession this year despite a drop in investment, productivity, wages and retail consumption amidst a national cost of living crisis. The Reserve Bank raised interest rates for the 13th time since May 2022 after, exacerbated by high fuel prices, inflation rose 1.2% in September.

Rate Trends Across APAC

Rates in Singapore, Sydney and Melbourne have remained relatively stable since April 2023, and our booking data predicts this stability will continue into 2024. YoY, a continued gradual rise in Sydney ADR is forecasted with rates for January 2024 being booked at £147 compared to £136 in January 2023.

Australia was our busiest country this quarter and we booked more cities and properties than in any other APAC market, up 25% YoY.

An upward trajectory of Tokyo ADR is forecasted going into 2024, with rates being booked at around £166 in January compared to £113 at the start of 2023 (a 46.9% YoY increase).

Our booking data shows average rates in Mumbai are £155.02 (August-September 2023) – up 32.3% compared to £117.18 for the same period in 2022.

Similarly in Delhi, ADRs are up 20.7% YoY from £113.81 (August-October 2022) to £137.34 for the same period in 2023.

Rates in China are showing a 21.9% decrease since last quarter, from £152.98 (May-July 2023) to £125.53 (August-October 2023). Although, ADR in Hong Kong started 2023 at £117 but we’re booking units for the start of 2024 at around £126.45.

![Americas globe icon]() North America, South America and Canada

North America, South America and Canada

Economic performance in this region is stronger than expected and the rise of interest rates is predicted to slow. Positively, stock markets have performed well in the last quarter and yields available on bonds have returned to levels not seen since before the financial crash of 2008.

The economy has avoided the predicted recession and unemployment levels are remaining low, according to Deloitte.

Meetings and events have been fuelling sector recovery worldwide, and key US cities like Chicago and Dallas will push corporate convention demand in 2024, says Amex GBT.

According to Turner and Townsend, six out of the ten most expensive cities to build in are in the US: New York City is top, followed by San Francisco in second, then Boston, LA, Chicago and Seattle take positions seven to ten. This could influence a decline in new supply in these areas.

Rate Trends Across the Americas

In our last Update, we predicted a large drop in Chicago ADR by the end of the year. November rates show a 27% drop to £129 since the highs of July, and booking data still forecasts a further 17% drop to £106 by the end of December.

Dallas ADR is sitting around £76 as we end 2023, but are forecast to rise by as much as 44% to £110 next summer in line with the predicted spike in corporate event demand.

New York City is also showing a decline, albeit less sharp than in Chicago, with ADR dropping 7% from £257 in July to £237 in December.

Rates in Toronto and Mexico are showing continued stability and are forecast to continue their plateau into 2024.

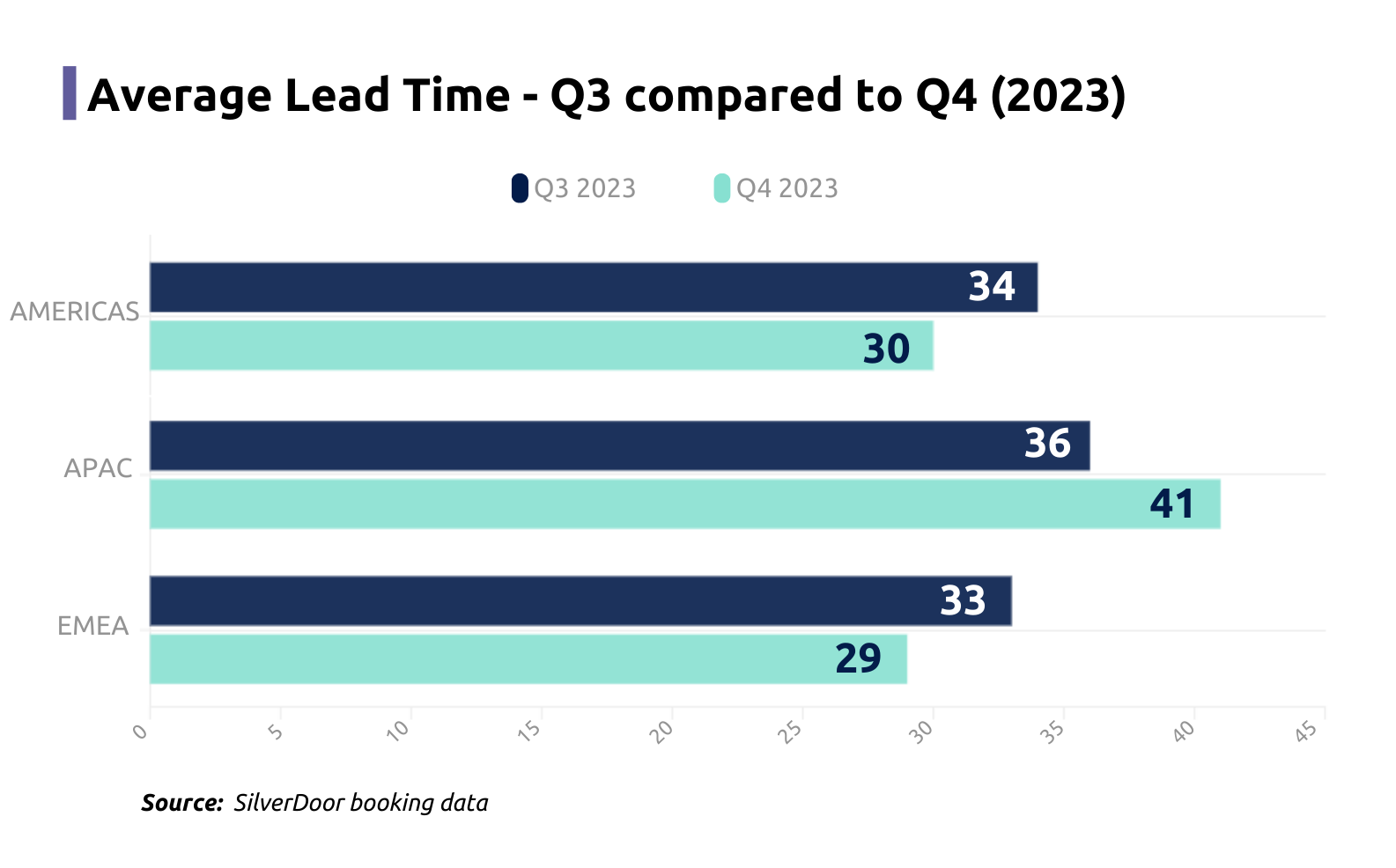

| Average length of stay (ALOS) in EMEA is 20.5% shorter for August-October 2023 compared to May-July. Demand tailing off towards the latter half of the year is pretty standard as peak relocation season has come to an end. ALOS in both the Americas and APAC, however, tells a different story and has extended by 22% and 19% respectively. This is still aligning with the industry trend of fewer trips but of a longer duration as travellers attempt to reduce the environmental impact of their business travel. Perhaps longer stays in the Americas are a result of the tightening of short-term rental legislation across key US, Canadian and South American markets as detailed in the latest GSAIR. |

|Supply trends we've noticed in the sector

There’s a notable investor, developer and consumer appetite for the branded residence accommodation model at the moment, particularly in the Middle East and moving into Europe. Savills reports an 150% growth of the segment in the last decade to nearly 800 branded residence projects and forecasts a further 50% growth by 2030.

Economy accommodation models are on the rise as they offer a well-rounded host of benefits for travellers, operators and investors: more guest flexibility; smaller but space-efficient units allow for more keys per sqm; and lower build costs in peripheral locations. ADR tends to be 15-20% lower in the growing economy segment.

Driven by an investor appetite for spreading risk and the growing traveller preference for co-living models, we can also expect to see more hybrid solutions and conversion projects. Conversion projects and economy models are an attractive investment given they are quick to market and can fit more units per sqm than luxury products.

_______________________________

Answer this quarter's quick poll!

AI is being incorporated into more and more aspects of hospitality. Which aspects of the booking journey do you see AI improving? Select all that apply.

- Enhanced customer service - e.g. better chatbots

- Streamlined booking process

- Tailored recommendations - e.g. accommodation or relevant add-ons

- Efficient complaint handling and resolution

_______________________________

|Events impacting supply, demand and pricing

|

|

Major annual and one-off events can increase rates and reduce availability. With bookings already being made for events throughout 2024, SilverDoor can advise on how to secure suitable accommodation at the best price.

If you would like specific topics or trends to be discussed in a future SilverDoor Market Update, get in touch with us at marketing@silverdoor.com.